Interest rates have gone down again. In fact, last week the benchmark 30-year fixed mortgage rate fell to 4.4 percent, the lowest point in over 13 months. I imagine you’ll be getting calls from your lender, banks, etc. about refinancing. This tends to happen when rates go down.

I have a confession: I think refinancing a mortgage is a bad idea.

There. I said it. I think we can find instances where refinancing makes sense. More often than not, refinancing comes at a tremendous cost to the homeowner. Today, I want to put some math behind behind my statement. And keep in mind, math and money are not the same (more on this below).

To better understand my position, we first have to understand how mortgages work.

Your mortgage payment = principal repayment (the amount borrowed) + interest payment (the interest charged).

Mortgages work a little differently than other loans. The interest is front loaded and principal repayment is backloaded. Advantage = lender. This makes sense from a lending perspective, though. The lender is taking all of the risk in lending the money.

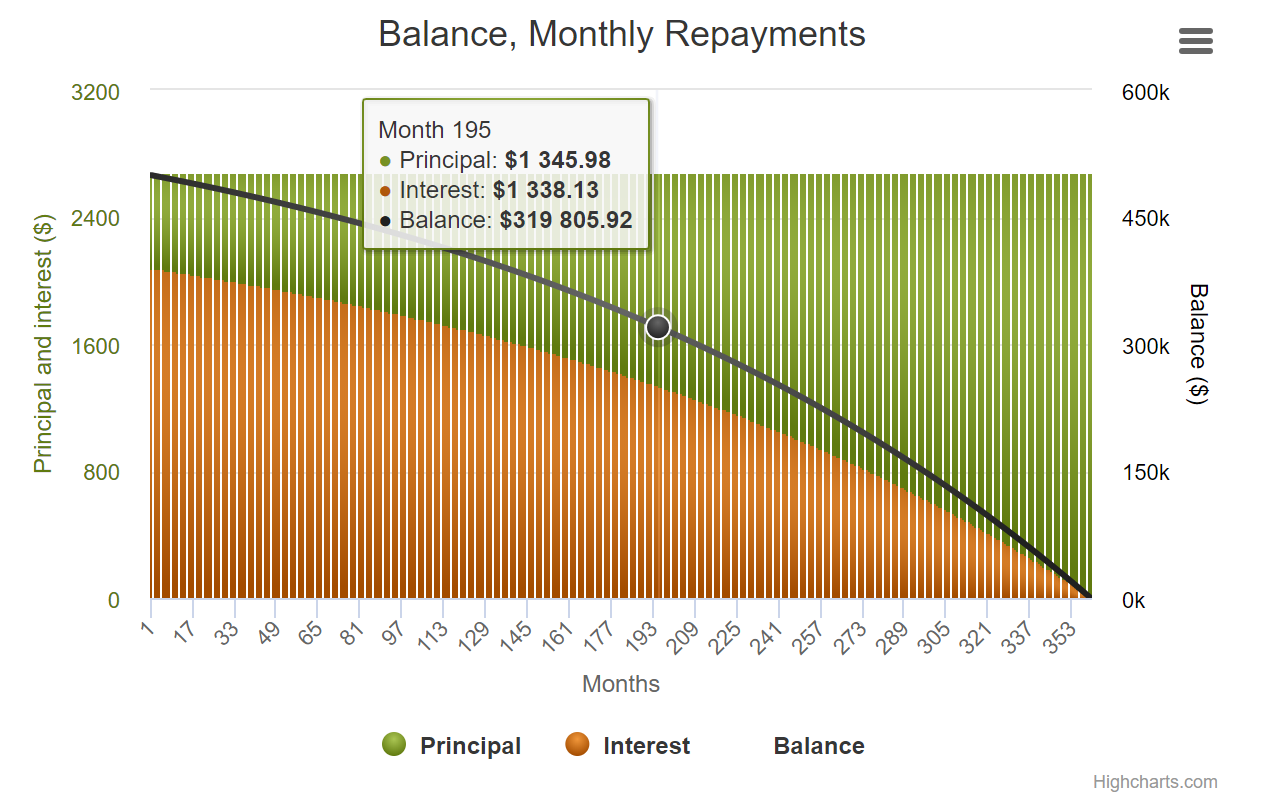

So let's set some parameters so we can better understand what's going on. Our loan is $500,000, our interest rate is 5%, and we'll go with a 30 year mortgage. This makes our monthly payment $2684.11.

Of that $2684.11, $2083.33 is interest payment and $600.77 is principal repayment in the first month (see above).

Woof.

Our chart to the left tells us it takes 195 months, or just over 16 years, before our principal repayment is greater than our interest payment. Double woof!

Now we know how the mortgage repayment works.

For a more detailed look, visit this fun website to run your own calculations.

And because we pay so much interest on the front end of a mortgage loan, refinancing tends to work in favor of the lender.

After 60 months of our original mortgage, we've already paid $120,190 in interest payments. Compare that to just ~$41,000 in principal repayments. Remember, our mortgage payment is frontloaded with interest payments so we're already down $120,190. That money is lost, gone forever, never to be seen again on our balance sheet.

Let's say five years from now interest rates have gone down (just like they did last week).

We owe $459,143 on our original loan still. And we can refinance at 4.25%. Even better, we can do so with $0 closing costs, escrow, etc. I like simple so our new loan amount is exactly what owe on our original loan. Sweet!

Our new payment is now $2258.71…even sweeter! Right?

Of course, because we've just lowered our payment by $425/month!! Some might say we've "saved" that amount. True, but only if we actually save it. More often than not it gets recaptured by lifestyle, but that's for another blog post.

Since we've already lost $120k to interest payments, this $425/month over the next 25 years has to be more than the interest we've already paid. I use 25 years (300 months) because our original mortgage would have been paid off by then. That's important to remember.

And a quick punch of my calculator:

$425 x 300 months = $127,500

$127,500 is more than $120,000 we've paid in interest already…boom!

But wait a second.

Remember, our original loan was going to be paid off in 30 years. We refinanced to a new 30 year mortgage 5 years in. Now we're paying our mortgage for 35 years in total. We have to add the final five years of our mortgage payments back into our equation.

That total = $135,522 ($2258 x 60 months)

Whether we want to look at the final five years of mortgage payments ($135,000) or count the lost mortgage interest on our initial mortgage ($120,000), refinancing is going to cost us at least an additional $120k or more.

The math here tells me - and hopefully tells you - refinancing rarely works out for the borrower. We end up deferring our mortgage payment out too far. We get enamored by the "savings" a refinance dangles in front of us. We pay too much mortgage interest up front. And not enough principal. And when we refinance, we start the cycle all over again. Because of the mortgage repayment schedule, it almost ALWAYS works out for the lender.

On the other hand, if you're disciplined enough to refinance AND invest the monthly payment *savings* then a refinance could be a smart move here. We can put compounding interest on our team and (most likely) come out ahead of the mortgage interest monster.

At the beginning of this post I said math and money aren't the same. Math is exact. There is always a right and a wrong answer. No in between.

Money on the other hand has very few if any right or wrong answers. It's wrought with gray areas. It's…emotional.

We tend to confuse the two when it comes to our financial lives. We run projections, like this one, that covers 30 years.

Can you tell me where you'll be in 30 years? I know I can't. Hell, ten years ago I didn't think I'd have 5 kids, let alone my own financial planning firm. So these projections? They look really really good on paper. From a math perspective, it all works out just so, right? But your life, your money? It might not.

You might want that $425/month to pay off higher interest student loans faster. You might need that $425/month to cover day care costs. You might need that $425/month to help a family member, start a business, or any number of other reasons. Why? Because it's personal.

If you're thinking about refinancing the math may say no but your personal situation might say something different. And that's the value of advice.

Either way, talk with your financial planner about it. Or schedule a time to talk with me.

PS - if you have private mortgage insurance (aka PMI), I won't get into the schematics of that scenario. I could, but our friends over at the Nerd's Eye View have done an outstanding job of discussing it in this blog post.