Only just recently did it start to feel like fall here in the DC Area. For a while it seemed like summer (and the rain) would never end. Now the leaves are starting to change colors and beginning to fall. Which means it really is autumn.

And as our 15 year old would say, "Wait. What?"

Seems like just yesterday the kids were finishing up with school and pool season was upon us. Then I blinked and summer was over. Now we have less than three months before the calendar turns over once again. Really? Already?!

Yes. Really.

Time really is flying by in our household. And I imagine many of you are experiencing the same phenomenon. Only it's not a phenomenon. This is what happens. Time waits for no man or woman. It just keeps going.

So today I want to talk about the importance of saving, and the impact of delaying our long term savings. We never really feel this impact, but it happens silently. And it happens over time. Oh yeah, and it's real.

You see, we get bombarded by our 401(k) provider, the financial pundits and peddlers, and other media outlets.

"Save while you're young."

"Get started TODAY!"

And so we might say to ourselves or our spouses, "You know, I should start saving" or "Let's save more money this year."

And then January turns into June. June turns into October. And then bam…HAPPY NEW YEAR!!!

Only we haven't saved more.

Wait. What?

I talk a lot about behavior and how it impacts our financial future. You can read some of them here (Stuck In a Rut) and here (the-secret-to-financial-success). Today I want to show you the impact of waiting to save, and what it really means to your financial future.

As my friend Joe taught me, we only get one compound curve. And what that means is we all only get one chance to take advantage of compound growth. And today I want to teach you about a FINANCIAL TRUTH that impacts each and every one of us.

TRUTH: For every FIVE years you delay saving for retirement, you are robbing from your future self roughly 33% of your retirement value.

Think about that for a second.

Okay good. Now get your math hat on and let's get started.

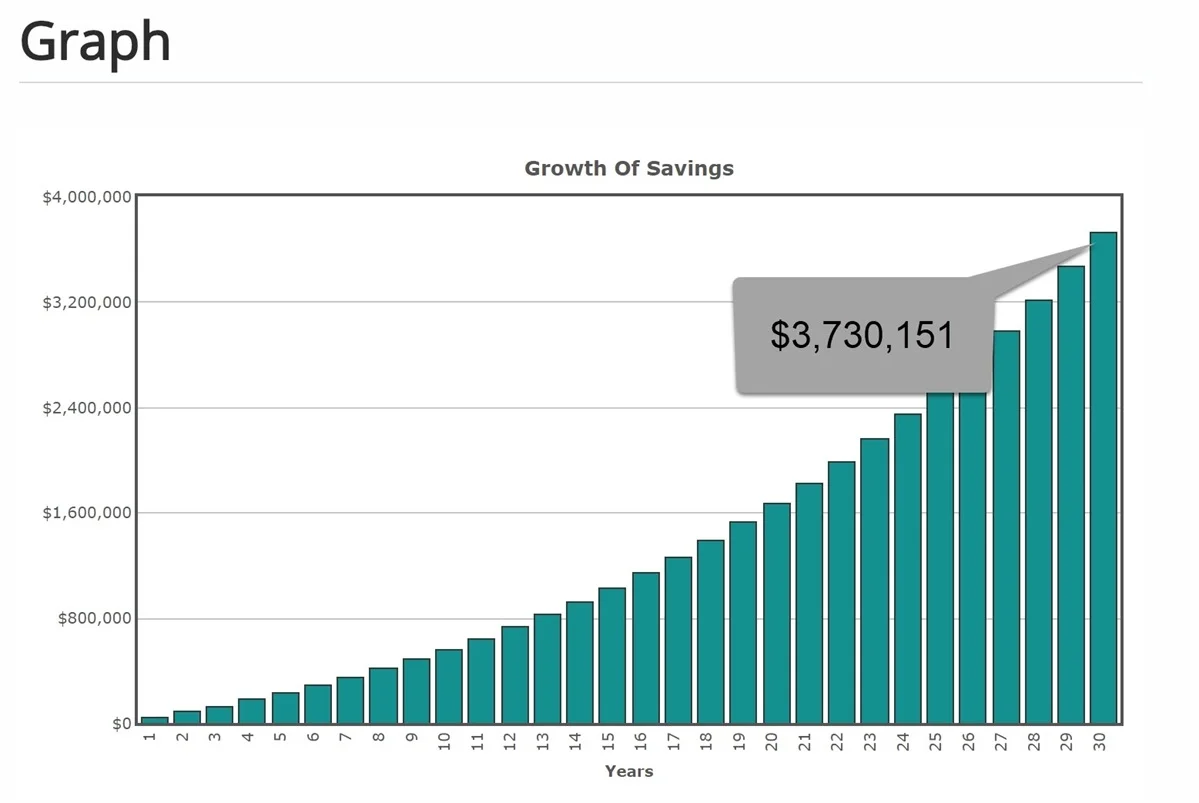

Here are my parameters. We're 35 years old. We earn $250,000 total household income and because we're excellent savers, we're able to invest 15% of our household income. In real dollars, that's $37,500 per year.

And we'll do that for the next 30 years, because, again, we're excellent savers. And let's also assume we're able to earn a very generous and very consistent 5% after tax rate of return on our money. And again, we can do that for 30 years.

In our money bubble to the left we can see we'll have roughly $3.7m by the time we're 65 years old. Not too shabby, right?

Now let's say we put off our decision to save for 5 years. Because time is FLYING by. And again, our FINANCIAL TRUTH says that for every 5 years we delay saving for retirement, we cost our future selves roughly 33% of our future value.

So doing the quick math, that would mean we'd have about $2,500,000 at age 65, or about $1.2m less. Drumroll, please…

Well, would you look at that. We delayed our retirement savings by 5 years which means now we're 40 years old when we begin to save for the future. And true to form, we have roughly $2.5m at age 65. Again, our FINANCIAL TRUTH holds true!

Let's keep it rolling though because this is getting fun.

Here's our next scenario. Time is literally flying by through our mid 30's/early-40's and we are spending every penny. Man, life is fun! Only now we're 45 years old and, yes, we're starting to feel the pressure. Now we're finally ready to start saving & investing for retirement. So if we're following our FINANCIAL TRUTH then we should again have 33% less money at age 65. Are you nervous? Are you excited? Let’s find out…

EGAD!

If we begin saving for retirement starting at age 45, then 20 years later we have roughly $1.6m.

And one more time, our $1.6m is again roughly 33% less money than we'd have if we started saving and investing at age 40 ($2,500,000 x 67% = $1,675,000).

Sidenote: This $1.6m is nothing to scoff at. That's a good sum of money in today's dollars. Keep in mind 3% inflation over 20 years would make $1.6m tomorrow feel like $800,000 today.

Okay, sidenote over and we're back.

If you haven't caught on just yet, here's a quick update - start saving (more) like NOW!

I could keep going here but I think you're pretty smart. You're picking up what I'm throwing down. However, I do want to talk about one more scenario.

Let's say our 45 year old self wants to have the same amount of money at age 65 as our 35 year old self. Is it possible?

It is!

It's going to take some serious work and discipline, though. In fact, I think our 45 year old self is going to have to save MORE THAN TWICE as much money for the next 20 years as our 35 year old self would have to save for 30 years. Let's see…

Over there on the right, our money bubble shows us our 45 year old self has stepped off into retirement with roughly the same pile of money as our 35 year old self (roughly $3.9m vs $3.7m).

Whew, we did it! But at what cost? The cost is we have to save 35% of our income each and every year. That's saving 20% more money per year than our 35 year old self, who was saving 15% of income. In dollars, that's $87,500 per year vs. $37,500.

Impossible? No. Likely? Also, no.

Here's why I think that.

You see, by the time we're 45 years old we are attuned and accustomed to a lifestyle. And not many people are ready to give up on that lifestyle.

Some of us, at this stage in life, might be fortunate to make significantly more money. Maybe we take a new job or position, or start a successful business. And with that higher income we could do it IF we didn't also adjust our lifestyle.

And that's a big "IF" - hence ALL CAPS. What it says to me is it's the very rare individual out there who can play retirement catch-up like our 45 year old self here just did. Most of us will not. And that's okay. It doesn't make you a bad person. It makes you human.

At this point, not all is lost. We simply have to adjust and adapt. Life is not a straight line. Neither is your financial life. But waiting until tomorrow or next week or next year isn't doing us any good. That's being an Ostrich.

So get started. Baby steps, do something small then build from there. And if you can't do it on your own or won't do it on your own then find someone to help you and hold you accountable for your financial future. Your future self will thank you for it.

And you might just have 33% more money in retirement than you thought!

Hypothetical examples are not intended to suggest a particular course of action or represent the performance of any particular financial product or security.